Why an FHA Loan migth the best for first time home buyers.

From financing the purchase of your first home to the coverage of additional repairs an FHA loan may be the option you've been looking for.

MONEYREAL ESTATE

12/7/20243 min read

FHA Loans: A Comprehensive Guide to Affordable Home ownership

The Federal Housing Administration (FHA) loan program is a popular choice for many homebuyers, particularly first-time buyers and those with less-than-perfect credit. Backed by the FHA, these loans are designed to make homeownership more accessible and affordable. Here's everything you need to know about FHA loans, their benefits, requirements, and how they compare to other mortgage options.

What is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration, a government agency under the U.S. Department of Housing and Urban Development (HUD). Established in 1934, the FHA was created to stimulate the housing market by making it easier for people to secure home financing.

Lenders issue FHA loans, but the government guarantees them, reducing the risk for lenders and allowing borrowers to qualify with more flexible terms.

Key Benefits of FHA Loans

1. Lower Down Payment Requirements

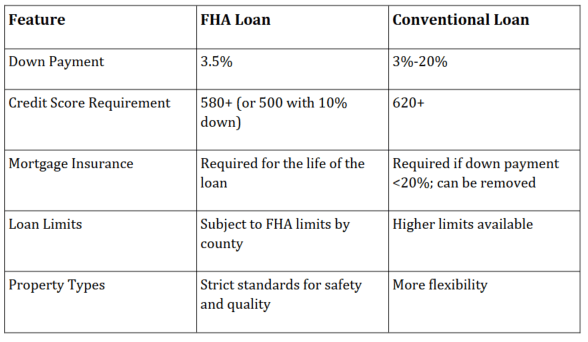

Borrowers can qualify with as little as 3.5% down, making FHA loans an attractive option for buyers with limited savings.

2. Flexible Credit Score Requirements

FHA loans are accessible to those with credit scores as low as 580 (or even 500 with a larger down payment). This makes them an excellent option for individuals working to rebuild their credit.

3. Competitive Interest Rates

Because FHA loans are government-backed, they often come with lower interest rates than conventional loans.

4. Assumable Loans

FHA loans are assumable, meaning a buyer can take over the seller's existing FHA loan, potentially benefiting from a lower interest rate.

5. Financing for Repairs

FHA 203(k) loans allow borrowers to finance the purchase of a home and its renovation costs in a single mortgage.

FHA Loan Requirements

To qualify for an FHA loan, borrowers must meet specific criteria:

1. Credit Score

- 580+ to qualify for a 3.5% down payment.

- 500–579 may qualify with a 10% down payment.

2. Debt-to-Income Ratio (DTI)

Typically, your DTI ratio should not exceed 43%, though exceptions may be made for strong applicants.

3. Mortgage Insurance : FHA loans require two types of mortgage insurance:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of the loan amount, paid at closing.

- Annual Mortgage Insurance Premium (MIP): Paid monthly, ranging from 0.45% to 1.05% of the loan amount, depending on the loan term and down payment.

4. Property Standards

The home must meet HUD’s minimum property standards, ensuring it’s safe, sound, and secure.

5. Primary Residence

FHA loans are only available for homes intended to be the borrower’s primary residence.

Who Should Consider an FHA Loan?

FHA loans are ideal for:

- First-Time Homebuyers: With low down payment and credit score requirements, FHA loans are an excellent choice for first-time buyers.

- Borrowers with Low Credit Scores: Those working to rebuild their credit can still achieve homeownership.

- Limited Savings: If you lack substantial savings for a down payment, an FHA loan can help bridge the gap.

How to Apply for an FHA Loan

1. Choose a Lender

Not all lenders offer FHA loans, so ensure you work with a lender approved by the FHA.

2. Get Pre-Approved

This involves verifying your income, credit, and financial history.

3. Find a Home

Work with a real estate agent to find a property that meets FHA guidelines.

4. Complete the Loan Application

Provide the necessary documentation, such as income statements, tax returns, and credit history.

5. Close on Your Loan

After the lender processes your application and the property is appraised, you’ll sign the final paperwork and move forward with your purchase.

Conclusion

FHA loans provide an accessible pathway to home ownership for many Americans. With low down payment requirements, flexible credit standards, and government backing, they make buying a home achievable even for those with financial challenges. However, it's essential to weigh the pros and cons, including mortgage insurance costs and property restrictions,

to ensure it’s the right fit for your needs.

If you’re considering an FHA loan, consult with an experienced lender to explore your options and take the first step toward owning your dream home.